Introduction and Overview

The National Pension Scheme (NPS) is a market-linked, low-cost, defined-contribution retirement system regulated by PFRDA. Launched in 2004 for government employees and extended to all citizens in 2009, NPS offers two account types—Tier I (retirement corpus with withdrawal restrictions) and Tier II (voluntary savings with free withdrawals). Investors can choose lifecycle-based auto allocation or Active Choice across Equity (E), Corporate Bonds (C), Government Securities (G), and Alternative Assets (A). Charges are among the lowest globally, and long-term compounding with disciplined contributions aims to build a retirement corpus.

Key Features at a Glance

- Regulator: Pension Fund Regulatory and Development Authority (PFRDA)

- Account types: Tier I (primary pension), Tier II (optional savings)

- Investment choices: Auto Choice (LC-75/50/25) or Active Choice (E/C/G/A with caps)

- Low costs: Fund management and admin charges are among the lowest

- Portability: Across jobs, locations, and fund managers

- Transparency: NAV-based daily valuation and online account access

- Liquidity: Partial withdrawals permitted under specified conditions

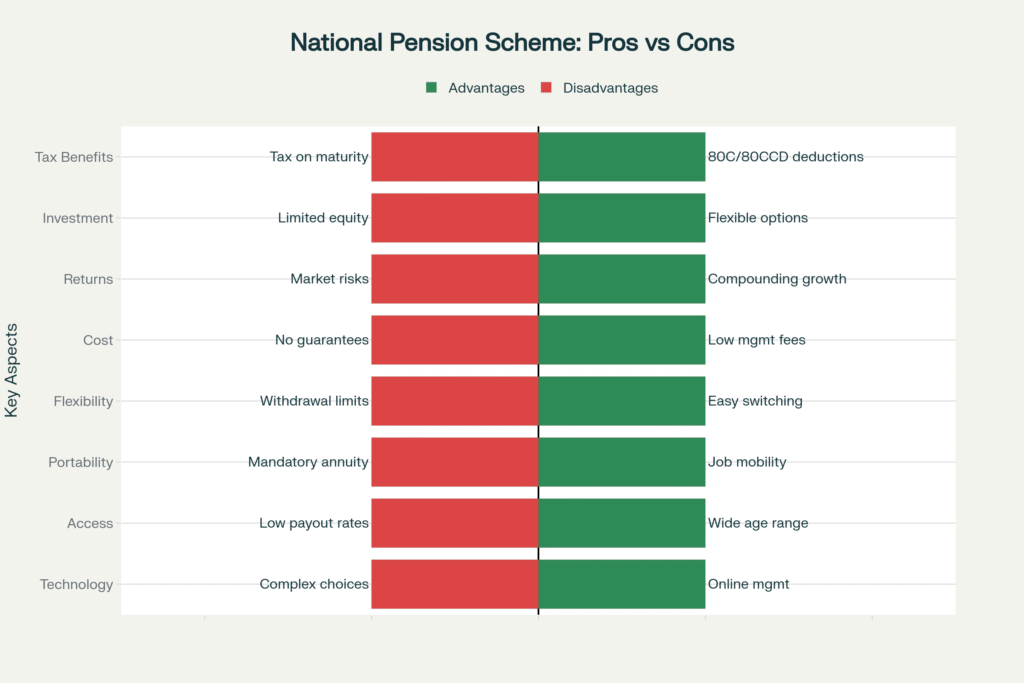

Pros vs Cons

| Pros | Cons |

|---|---|

| Low cost structure improves net returns over long horizons | Market-linked—returns are not guaranteed |

| Tax advantages under 80C, 80CCD(1B) and 10(12A) | Mandatory annuitization at exit for Tier I |

| Professional fund management by licensed PFMs | Equity cap limits may constrain aggressive investors |

| Flexible asset allocation (Auto/Active) | Partial withdrawal and exit rules add complexity |

| Portability across employers and states | Lock-in until age 60 (Tier I) |

| Transparent, regulated product with online access | Annuity income taxed as per slab in retirement |

Eligibility and Account Types

- Who can join: Indian citizens (resident/non-resident) and OCI, age 18–70; KYC required.

- Tier I: Primary retirement account. Minimum contribution typically Rs 500 per contribution and Rs 1,000 per year (as guided by PFRDA; POPs may specify operational thresholds). Tax benefits available.

- Tier II: Optional savings account with free withdrawals; no tax benefits for general citizens (certain benefits for central government employees subject to rules).

- Corporate NPS: Employers can contribute on behalf of employees with separate tax rules.

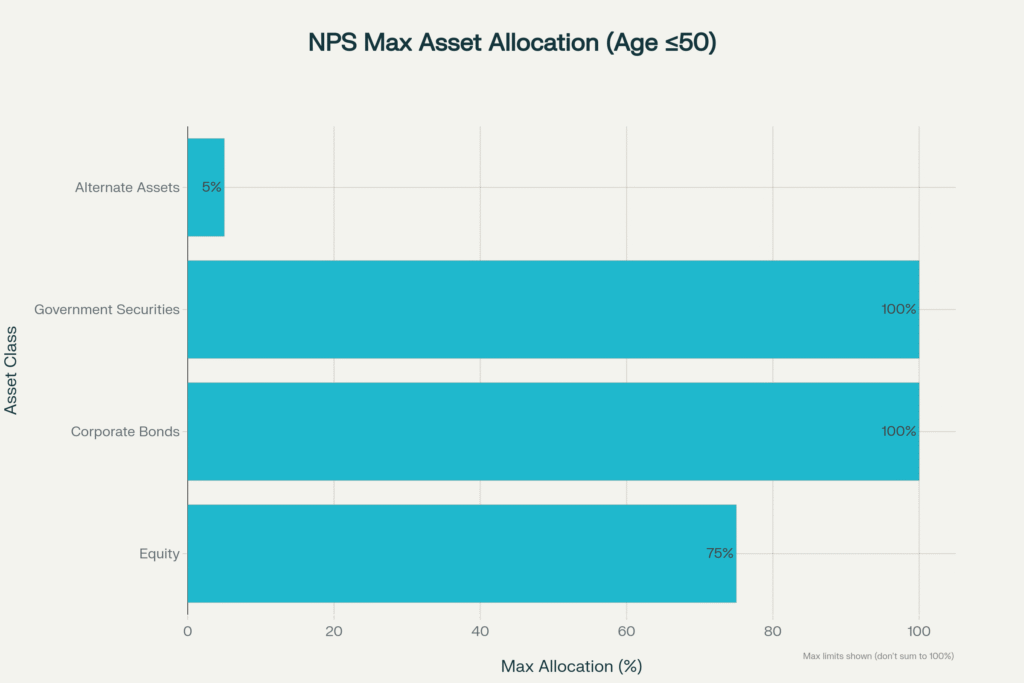

Investment Choices and Asset Allocation

- Auto Choice: Lifecycle funds that reduce equity exposure with age (LC-75 Aggressive, LC-50 Moderate, LC-25 Conservative).

- Active Choice: Investor selects E/C/G/A subject to caps (E typically capped at 75% for citizens; A capped lower). Rebalancing allowed; switch PFMs and schemes as needed.

- Performance: Historically, diversified NPS schemes have delivered competitive long-term returns; past performance does not guarantee future results.

Tax Benefits (as per prevailing provisions; verify latest rules)

- Section 80CCD(1): Within overall 80C limit of Rs 1.5 lakh—employee/self-contribution subject to 10% of salary (20% of gross income for self-employed).

- Section 80CCD(1B): Additional exclusive deduction up to Rs 50,000 for NPS Tier I.

- Section 80CCD(2): Employer’s contribution up to 10% of salary (14% for central government) deductible, subject to overall limits.

- At Exit (Section 10(12A)): Up to 60% of corpus withdrawable tax-exempt; minimum 40% to be used to buy an annuity (annuity income taxable).

- Partial Withdrawal (Section 10(12B)): Up to 25% of own contributions for specified purposes after 3 years, subject to limits.

Withdrawals, Exit and Annuity Rules

- Normal exit at 60: Up to 60% lump sum tax-free; at least 40% for annuity. Option to defer withdrawal and continue contributions up to age 70.

- Premature exit (before 60): Up to 20% lump sum; at least 80% annuitized, subject to minimum corpus thresholds.

- Partial withdrawals: Education, marriage of children, purchase/construction of first house, specified illnesses, etc., after meeting criteria.

- Annuity options: Immediate annuity, with/without return of purchase price, joint-life variants; choose IRDAI-regulated annuity provider.

Best Practices for NPS Investors

- Start early to maximize compounding; contribute regularly via SIP-like scheduling.

- Choose Auto Choice unless you actively monitor markets and rebalance.

- Maintain equity within comfort for volatility; consider lifecycle glide-path.

- Review PFM performance annually; switch if consistent underperformance.

- Align NPS with other retirement assets (EPF/PPF/mutual funds) for holistic allocation.

- Plan annuity selection well before retirement; compare rates and features.

- Keep nominee details and contact information up to date.

Frequently Asked Questions

- Can NRIs invest? Yes, subject to FEMA and KYC; OCI eligible; PIO no longer eligible unless otherwise specified by PFRDA.

- What are costs? Low fund management fees (basis points), plus small record-keeping and POP charges.

- Can I have multiple NPS accounts? Only one PRAN across India; portable.

Conclusion

NPS is a regulated, low-cost, long-horizon retirement solution that complements EPF/PPF and mutual funds. With disciplined contributions, prudent asset allocation, tax benefits, and strong oversight, NPS can be a core component of a diversified retirement plan, particularly for investors seeking structured, goal-based investing with transparency and portability.

Leave a Reply